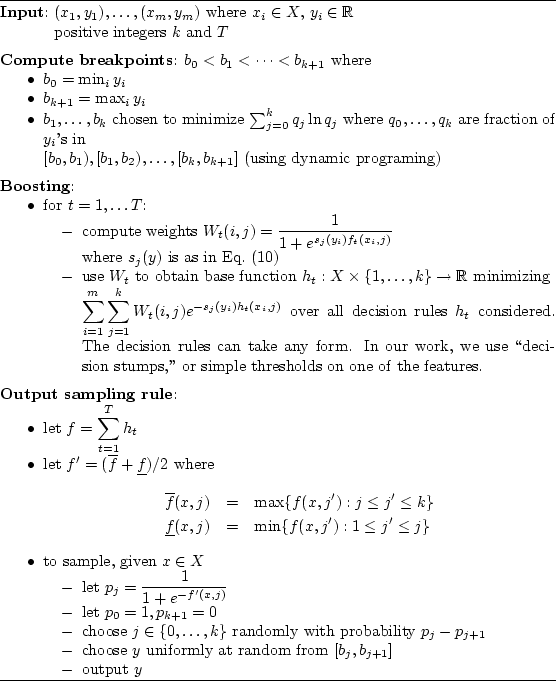

Having described how we set up the learning problem, we are now ready to describe the learning algorithm that we used. Briefly, we solved this learning problem by first reducing to a multiclass, multi-label classification problem (or alternatively a multiple logistic regression problem), and then applying boosting techniques developed by Schapire and Singer SchapireSi99,SchapireSi00 combined with a modification of boosting algorithms for logistic regression proposed by Collins, Schapire and Singer CollinsScSi02. The result is a new machine-learning algorithm for solving conditional density estimation problems, described in detail in the remainder of this section. Table 5 shows pseudo-code for the entire algorithm.

Abstractly, we are given pairs

![]() where each

where each

![]() belongs to a space

belongs to a space ![]() and each

and each ![]() is in

is in

![]() .

In our case, the

.

In our case, the ![]() 's are the auction-specific feature vectors

described above; for some

's are the auction-specific feature vectors

described above; for some ![]() ,

,

![]() . Each target quantity

. Each target quantity

![]() is the difference between

closing price and current price.

Given a new

is the difference between

closing price and current price.

Given a new ![]() , our goal is to estimate the conditional distribution

of

, our goal is to estimate the conditional distribution

of ![]() given

given ![]() .

.

We proceed with the working assumption that all training and test

examples ![]() are i.i.d. (i.e, drawn independently from identical

distributions).

Although this assumption is false in our

case (since the agents, including ours, are changing

over time), it seems like a reasonable approximation that greatly

reduces the difficulty of the learning task.

are i.i.d. (i.e, drawn independently from identical

distributions).

Although this assumption is false in our

case (since the agents, including ours, are changing

over time), it seems like a reasonable approximation that greatly

reduces the difficulty of the learning task.

Our first step is to reduce the estimation problem to a classification

problem by

breaking the range of the ![]() 's into bins:

's into bins:

For each of the breakpoints ![]() (

(![]() ),

our learning algorithm attempts to

estimate the probability that a new

),

our learning algorithm attempts to

estimate the probability that a new ![]() (given

(given ![]() ) will be at least

) will be at least

![]() .

Given such estimates

.

Given such estimates ![]() for each

for each ![]() , we can then estimate the

probability that

, we can then estimate the

probability that ![]() is in the bin

is in the bin ![]() by

by ![]() (and we can then use a constant density within each bin).

We thus have reduced the problem to one of estimating multiple

conditional Bernoulli

variables corresponding to the event

(and we can then use a constant density within each bin).

We thus have reduced the problem to one of estimating multiple

conditional Bernoulli

variables corresponding to the event ![]() , and for this, we use

a logistic regression algorithm based on boosting techniques as

described by CollinsScSi02 CollinsScSi02.

, and for this, we use

a logistic regression algorithm based on boosting techniques as

described by CollinsScSi02 CollinsScSi02.

Our learning algorithm constructs a real-valued function

![]() with the interpretation that

with the interpretation that

We attempt to minimize this quantity for all training examples

![]() and all breakpoints

and all breakpoints ![]() .

Specifically, we try to find a function

.

Specifically, we try to find a function ![]() minimizing

minimizing

When computed by this sort of iterative procedure,

CollinsScSi02 CollinsScSi02 prove the asymptotic convergence

of ![]() to the minimum of the objective function in

Equation (11) over all linear combinations of the base

functions. For this problem, we fixed the number of rounds to

to the minimum of the objective function in

Equation (11) over all linear combinations of the base

functions. For this problem, we fixed the number of rounds to

![]() . Let

. Let ![]() be the final predictor.

be the final predictor.

As noted above, given a new feature vector ![]() , we compute

, we compute ![]() as in

Equation (9) to be our estimate for the probability that

as in

Equation (9) to be our estimate for the probability that

![]() , and we let

, and we let ![]() and

and ![]() . For this to make

sense, we need

. For this to make

sense, we need

![]() , or equivalently,

, or equivalently,

![]() , a condition that may not

hold for the learned function

, a condition that may not

hold for the learned function ![]() . To force this condition, we

replace

. To force this condition, we

replace ![]() by a reasonable (albeit heuristic) approximation

by a reasonable (albeit heuristic) approximation ![]() that

is nonincreasing in

that

is nonincreasing in ![]() , namely,

, namely,

![]() where

where

![]() (respectively,

(respectively, ![]() ) is the pointwise minimum

(respectively, maximum) of all nonincreasing functions

) is the pointwise minimum

(respectively, maximum) of all nonincreasing functions ![]() that

everywhere upper bound

that

everywhere upper bound ![]() (respectively, lower bound

(respectively, lower bound ![]() ).

).

With this modified function ![]() , we can compute modified

probabilities

, we can compute modified

probabilities ![]() . To sample a single point according to the

estimated distribution on

. To sample a single point according to the

estimated distribution on

![]() associated with

associated with ![]() , we choose bin

, we choose bin

![]() with probability

with probability ![]() , and then select a

point from this bin uniformly at random. Expected value according to

this distribution is easily computed as

, and then select a

point from this bin uniformly at random. Expected value according to

this distribution is easily computed as

Although we present results using this algorithm in the trading agent context, we did not test its performance on more general learning problems, nor did we compare to other methods for conditional density estimation, such as those studied by Stone94 Stone94. This clearly should be an area for future research.